-(2)-(1).jpg)

What key changes have occurred in the Russian consumer market over the past six months? Is price still the deciding factor for consumers when purchasing products? We present to your attention the results of a new B1 survey.

SURVEY FINDINGS

-

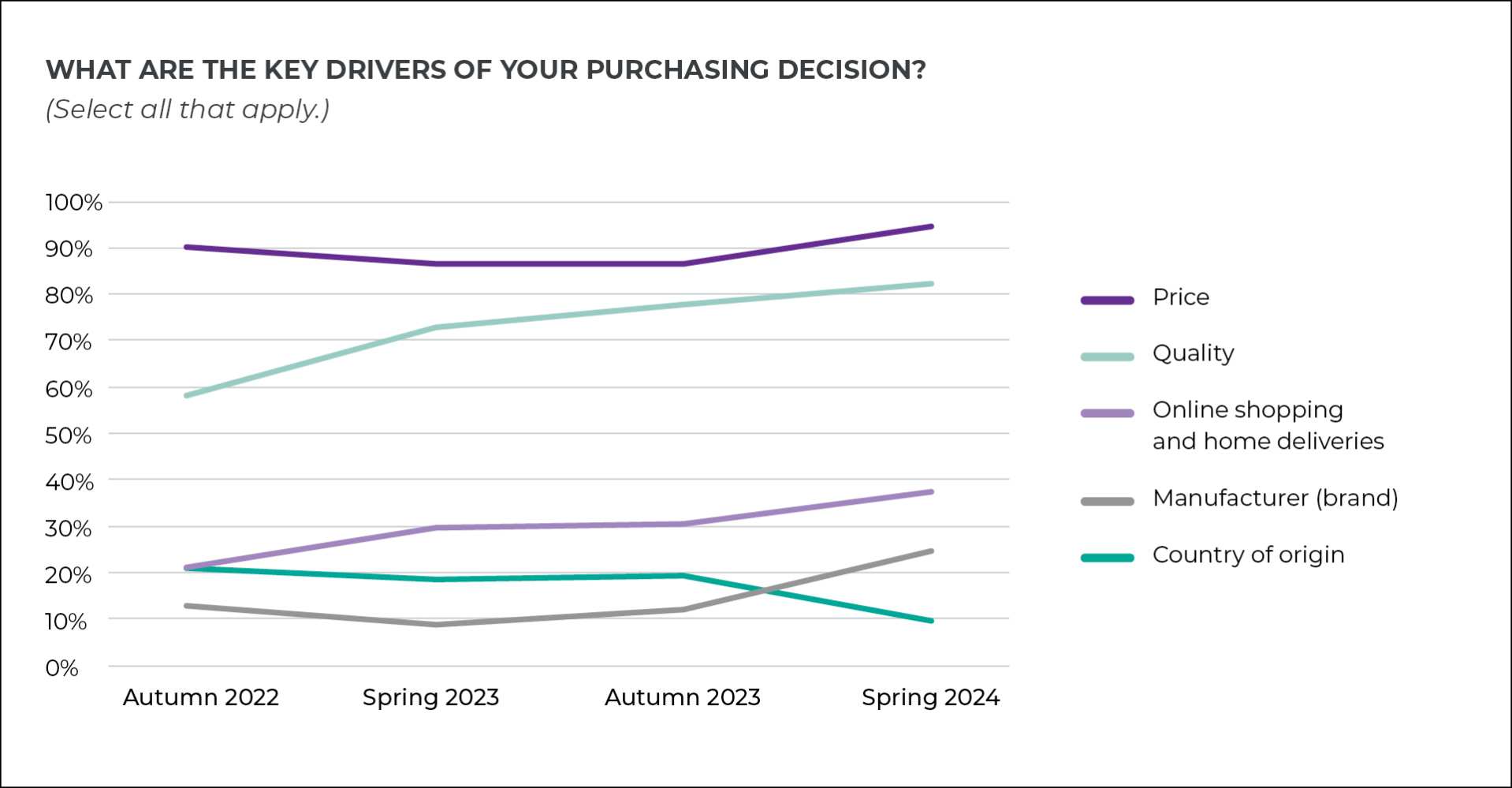

As many as 95% of respondents cited price as the primary factor influencing their purchasing decision, with 82% emphasizing quality — a 9 p.p. surge since autumn 2023

-

The majority of respondents have managed to find substitutes for products of the ‘departed’ brands, but the quality of these replacements often falls short compared to the original products, as reported by 60% of respondents (16% more than in the fall of 2023)

-

Most of the surveyed consumers are still unwilling to pay a premium for their accustomed brand items. However, those who do are enticed by the superior quality these products offer

-

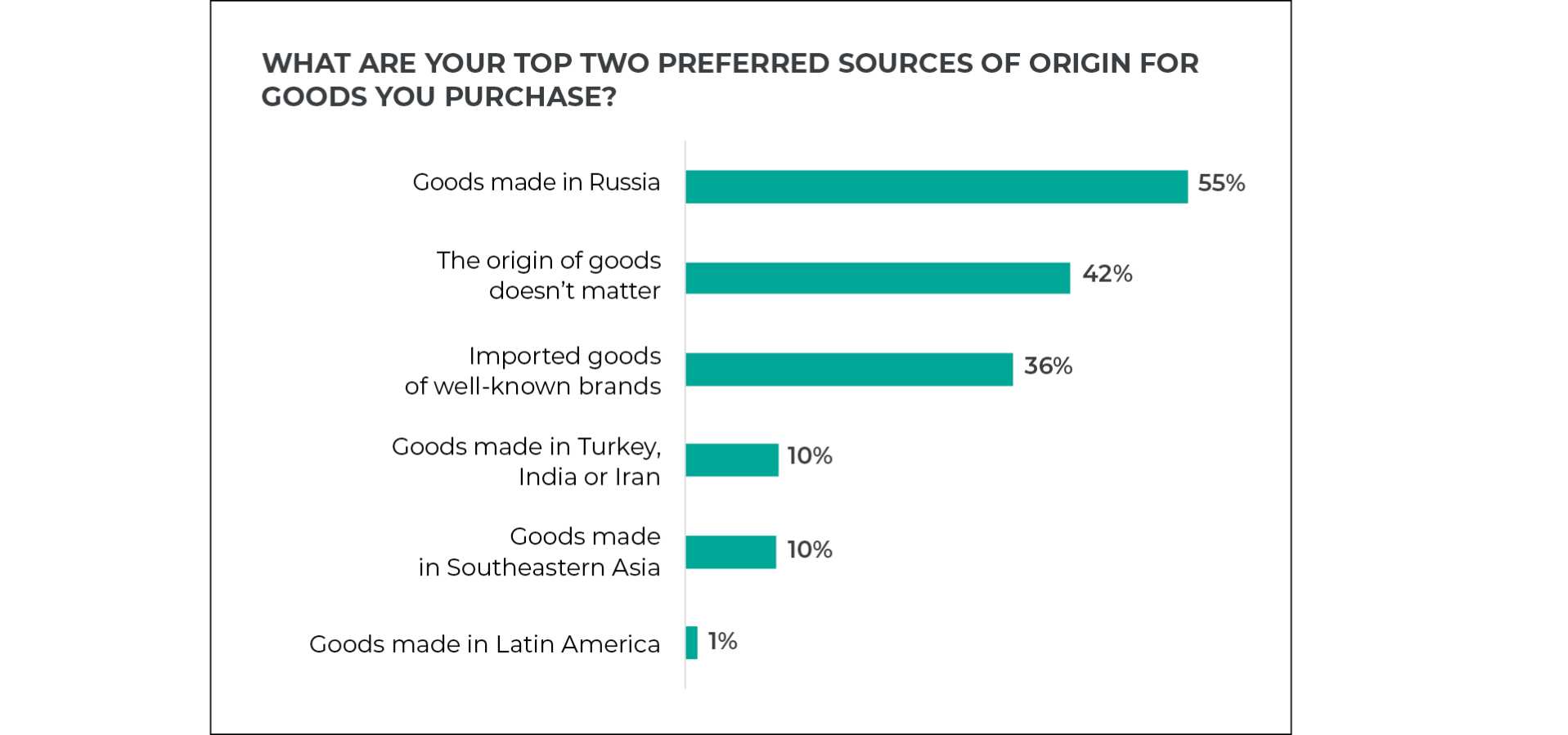

Russian-made goods are becoming increasingly popular (as reported by 55% of respondents) partly due to their growing variety

-

E-commerce is emerging as the main sales channel for non-grocery items, as reported by 93% of respondents; groceries are still mostly purchased offline

-

The surveyed consumers perceive a slight decline in the quality of private label products offered by retail chains

-

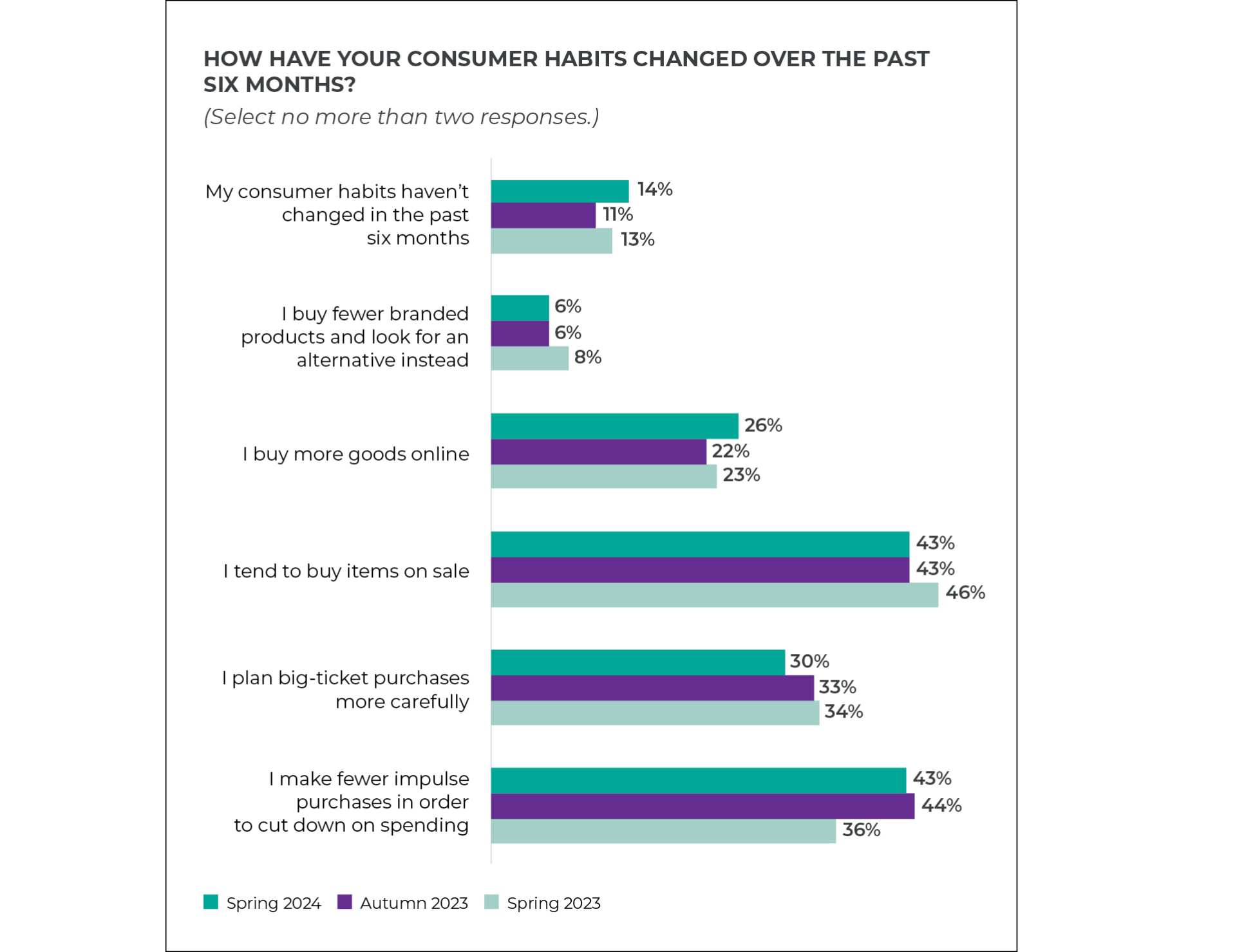

While the majority of respondents do not anticipate a shortage of consumer goods, they are not planning any big-ticket purchases in the next six months either

-

Older consumers are predictably less inclined towards embracing online delivery services and self-checkout options

-

Food and staples have climbed up the consumer priority list since last autumn, with both quality (from 75% to 80%) and price (from 75% to 79%) gaining significance in spring 2024

QUALITY AND PRICE ARE STILL THE TOP PRIORITIES WHEN MAKING A PURCHASE

When selecting a product, the consumers we have surveyed still focus mainly on price and quality.

Following closely behind, 82% emphasized quality. This suggests that consumers are looking for the best quality at an affordable price. Only 25% consider the brand to be the key driver of their purchasing decision, while 9% prioritize the country of origin.

The importance of quality and the ability to purchase online is also growing: in the fall of 2022, 58% of respondents cited the quality of goods as a decisive factor influencing their purchasing decision, and in the spring of 2024 – 82% of respondents, the ability to purchase online was named a decisive factor by 21% and 37%, respectively.

BRAND SUBSTITUTION HAS PROVED A VIABLE OPTION

As in previous surveys, we asked consumers to rate the availability of their accustomed products and brands. Among our respondents, 59% reported no change in availability, while the number of those who found their preferred items and brands unavailable, leading them to seek alternatives, has decreased from 44% to 25% since autumn 2022. In addition, 60% of surveyed believed that the replacement fell short in terms of quality.

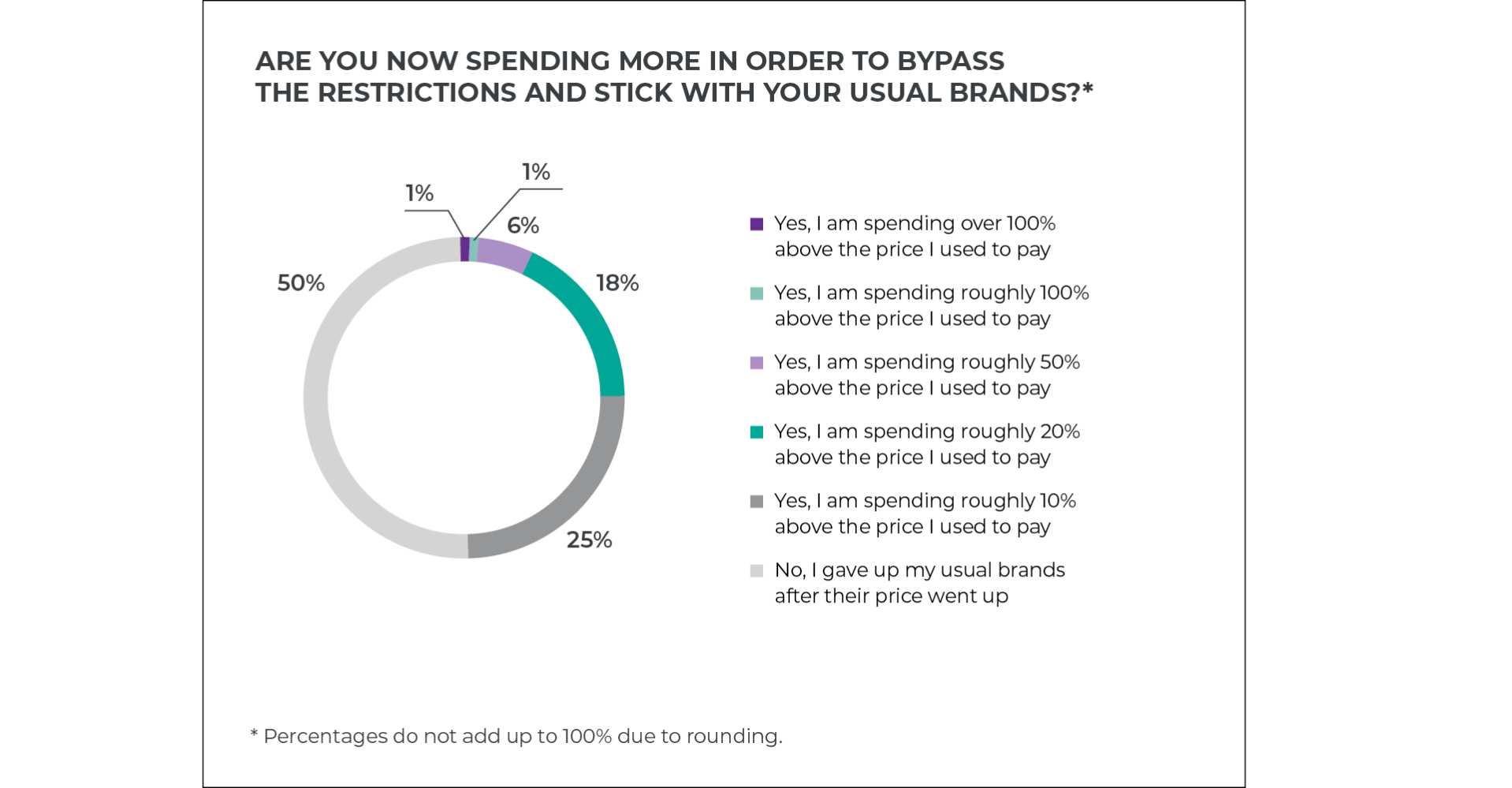

MOST CONSUMERS REMAIN RELUCTANT TO SPLURGE ON THEIR FAVORITE BRAND ITEMS

The vast majority of respondents in our survey continue to resist paying extra to stay loyal to their preferred brands: 50% have opted out of more expensive items. However, this reluctance has been steadily declining since spring 2023, when it was at 55%. Meanwhile, the number of those willing to spend up to 20% on top of the current price has increased from 13% to 18%. The two main reasons why most survey participants would be willing to pay a premium for certain brand items remain the high quality level (54%) and the challenge of finding substitutes (51%).

Interestingly, the younger the respondents, the greater their emphasis on quality. Among those under 24 years of age, 69% are willing to pay extra for high-quality products. Moreover, brand prestige matters more in this demographic: while 8% of all respondents prioritize it, among those under 24, it is 16%. The proportion of those willing to pay for superior quality has risen from 36% in autumn 2022 to 54% in spring 2024.

RUSSIAN GOODS CONTINUE TO REIGN SUPREME

Similar to our previous surveys in 2022 and 2023, most respondents continue to favor products made in Russia.

However, the appeal of well-known brands has declined over the past 18 months, dropping from 62% to 36%, partly due to scarcity of these items in the market. It is worth mentioning that in younger demographics, there is less concern about a product’s country of origin.

WHERE PEOPLE SHOP FOR GROCERIES VS. NON-GROCERIES DIFFERS

Based on our findings, most of the consumers we have surveyed prefer different shopping formats for groceries and non-groceries.

Non-grocery items are purchased on marketplaces by 93% of those surveyed, while 91% buy them through online classifieds, and 82% directly from suppliers’ online stores. For groceries, the proportion of online purchases is smaller. Major retail chains are the go-to for grocery shopping, with 94% of respondents making their purchases there, while 87% turn to local convenience stores and only 26% buy on marketplaces.

Interest in private label products has seen a slight decline among survey participants compared with six months ago. In both spring and autumn 2023, 54% of respondents regularly purchased these items. However, by spring 2024, this percentage had dropped to 48%. Meanwhile, there has been a gradual increase in the number of respondents perceiving the quality of such goods as subpar, leading to less frequent purchases. In spring 2023, this group constituted 25% of respondents, but by spring 2024, it had risen to 30%. This indicates that amid the prevailing trend favoring quality products at reasonable prices, respondents are becoming increasingly dissatisfied with the quality of private label offerings.

CONSUMER SENTIMENT IS TAKING A SLIGHT DIP

The appetite for big-ticket purchases remains modest among respondents, hovering below a third. It has decreased slightly over the past six months, from 32% in autumn 2023 to 27% in spring 2024.

The consumer habits of our respondents have seen only minor changes from previous survey waves.

However, when it comes to expectations regarding future offerings, optimism prevails. Among those surveyed, 70% expect that the supply of their usual goods and services will remain robust in the coming year, albeit this figure has seen a slight dip – by 4 p. p. since autumn 2023.

CONSUMERS CONTINUE TO SHIFT AWAY FROM BRANDS, EXPECTING NO CHANGE IN PRODUCT AVAILABILITY

As in previous survey waves, we have asked respondents to identify categories where they switched from a well-known brand to a Russian one or two products from an unknown manufacturer. Just like six months ago, the top three were casual clothing (30%), refreshments (28%), and tea and coffee (26%).

However, we are seeing mixed trends across categories compared with the last wave: in some, the share of people ditching big brands has grown (especially in refreshments (8 p. p.), chocolate (4 p. p.) and personal care products (3 p. p.)), while in others, it has decreased (by 4 p. p. in denim products and by 3 p. p. in fashion accessories, engine oils and car care products, and sports apparel). Nevertheless, in both cases, the percentage changes from the total number of respondents are not dramatic, indicating overall stabilization in the consumer market.

DELIVERY SERVICES ON THE RISE, MANUFACTURER PROMOTIONS LEAVE CONSUMERS SATISFIED

Consumers are increasingly tapping into these services (49%), with 11% favoring non-food items, 15% preferring groceries and 23% exploring all product types. The older generation has been slower to adopt, with 62% of respondents aged over 55 yet to embrace these conveniences.

According to our survey, retail promotional campaigns generally please consumers: 61% always shop the deals, satisfied with both quality and price. However, 9% are frustrated over sudden price hikes after the promotion ends.

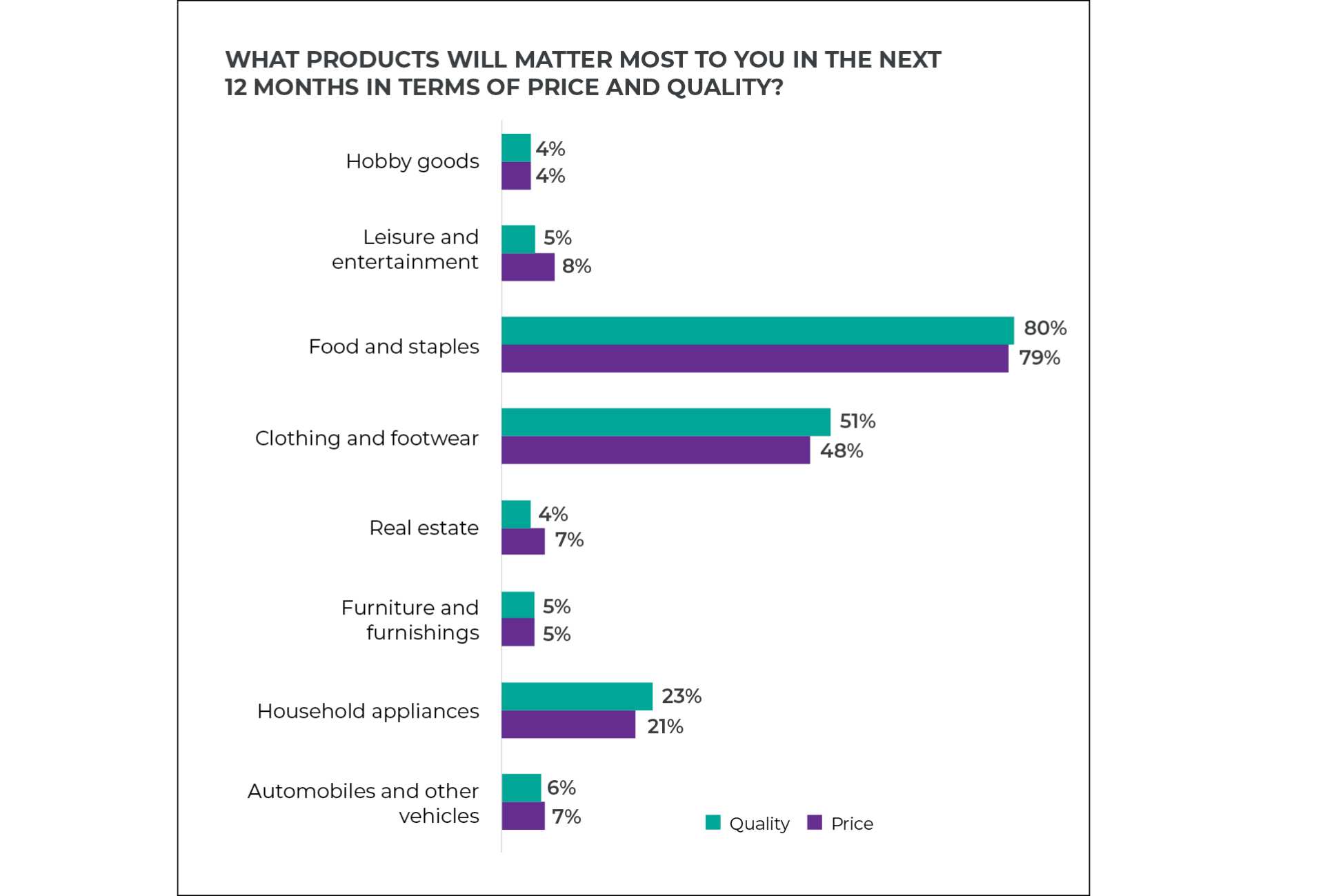

FOOD AND STAPLES HOLD STRONG: THEIR PRICE AND QUALITY REMAIN PARAMOUNT

Since autumn 2022, there has been a noticeable shift in priorities: the importance of clothing and footwear has decreased, dropping from 59% to 51% in terms of price and from 56% to 48% in terms of quality. On the other side, the significance of food and staples has risen, climbing from 75% to 80% in terms of price and from 75% to 79% in terms of quality. Furthermore, both price and quality remain important factors in these categories for men and women of all age groups.

-(2)-(1).jpg)

Our Contacts

Ilya Ananyev

B1 Partner

Assurance, Retail & Consumer Products, Agribusiness, Life Sciences and Pharma Leader

Contact

-(1).jpg)

Alexei Malenkin

B1 Partner

Retail & Consumer Products, Agribusiness and Life Sciences Tax Leader

Contact

.png)

Elena Tsaturova

B1 Partner

M&A and Restructuring Leader, Consulting, Technology and Transactions

Contact